Cash flow forecasting is a key skill that every small business owner should have. Because even if your business is profitable, it can still fail if you do not manage your cash flow well.

Why is cash flow forecasting important for small businesses?

Some of you tell me, “Tonia, I have no need for cash flow forecasting because I know how much money I am making each month.” Other entrepreneurs tell me, “Tonia, I have no need for cash flow forecasting because I struggle to make a profit every month.”

My answer to each of you: you still need to do cash flow forecasting.

Even if your business is doing so well that you do not worry about money at all, a cash flow forecast will help you gain a better understanding of your business. Why? Because it shows you how money is moving in your business. It helps you understand the patterns and the rhythm of your business.

If you do not understand the patterns in your business, you are like a tourist in a small boat on a big sea. Sure, you are enjoying yourself as long as the waves are not too high, the sun is shining and the light breeze is cooling your skin. But how will you respond when the storm comes?

Fishermen study the sea, the wind and the sky. They know when fish will be plentiful and they know where to find the best fish. They know how to avoid dangerous currents and sand banks.

They also know how to interpret what is happening. If the size of the waves is increasing, they know whether it means, “Go home now!” or “More fish are coming!”. They have mastered the rhythm and patterns of the sea.

Frankly, I believe that any business owner should master their business. This means that you understand the specific patterns in your business. For example: when are your expenses at their highest point (and why)? Or, what is the ebb and flow of your sales? This information will then tell you how to act.

Every business has its own patterns.

It is fine by me if your business strategy is to not study these patterns. But then please do not complain when the storm comes and you realise that you do not understand the waves and you cannot see the shore.

However, if you want to understand your business patterns, cash flow forecasting can help.

How can cash flow forecasting help a small business?

As a business, you can use cash flow forecasting for the following:

- Understand patterns of cash flowing into and out of your business

- Understand when you need to constrain your expenses

- Understand when you look to look for ways to increase the amount of money flowing into the business

- Understand when you will need to add money to the business

- Have more control over your business finances

How to do cash flow forecasting for small business

If you are a regular follower of my blog, you already know how to calculate your net profit. Doing cash flow forecasting is similar to calculating your net profit.

The main difference is that your profit calculation is like the rear-view mirror in a car. It tells you how your business performed during the past year. Cash flow forecasting is like a car’s wind shield. It shows you what is happening in front of you right now and what will happen in the next few weeks or months.

When you start forecasting your cash flow, I advise you to start on Day 1 of the new month. You can start with a one-month cash flow forecast, 3 months, or 1 year. One month will give you an idea of what to expect in the next few weeks, but you cannot use it to determine patterns in your business. A 3-month forecast will give you a better understanding.

I believe that 12 months is best, but if you are not familiar with cash flow calculations, I advise you to start with 3 months. After you feel confident that you fully understand it, you can expand it to 6 months and then to 12 months.

Step 1: determine your cash inflow

Data that you need: your sales forecast for the coming year and an overview of how much additional cash you expect to receive in each month.

Cash receipts include cash that you are expecting to receive from sales, cash that you are expecting to collect from customers who bought on credit, any loan or personal cash that you will add to the business, any cash that will come in from the sale of assets, and any other cash that may flow into the business.

Step 2: determine your cost of sales

Data that you will need: Your cost of sales is the money you paid to buy or produce the products or services that you sell. It is also called the Cost of Goods sold (COGS).

If you are a manufacturer, this is the money that you spent to produce the products that you are selling in your business. If you are a retailer, this is the money that you spent to buy your goods from suppliers.

Don’t forget to include transportation and – if you are a manufacturer – salaries paid to any production staff. Check out this blog post for a step-by-step explanation of how to calculate COGS.

Step 3: determine your business expenditure

Data that you will need: All your business expenses that you are expecting for the coming year. For this step, we are only interested in your business expenses.

If you are not sure about your business expenses, guess. Then use your recordkeeping to get a good overview of how much money your business is spending every month.

Step 4: determine your cash or capital withdrawals

Data that you will need: the cash or capital withdrawals include your personal expenses, whether you took a personal loan from your business, and other withdrawals that you did. It also included the purchase of assets.

Assets are purchases that last for an extended period of time. They are things that you control and that you can use to generate profit today and in the future. Examples of assets include office furniture, production equipment, vehicles for business use or a laptop.

Things that are not assets: pens, paper, cartridges for printers. These are everyday business operating expenses.

In my own consultancy, the rule of thumb that I use to determine whether something is an asset or not: it should cost more than €900 and I have to be able to use it for at least 3 years. If it does not meet these criteria, it is a business expense. Note: your criteria may be different.

Step 5: determine cash on hand

Data that you will need: the amount of cash on hand on Day 1. So if your forecast is starting on June 1st, note the cash on hand at Close of Business on May 31st. (Or, before start or business on June 1st.)

This includes cash on hand in the business and cash in the bank account. Do not include your savings if you have a separate business savings account.

Step 6: determine total cash outflow

Add up the total of your cost of sales (step 2), your businesses expenses (step 3) and your cash or capital withdrawals (step 4). The total amount is the total cash outflow in any given month.

Step 7: determine net cash flow

Subtract your total cash outflow (step 6) from your total cash inflow (step 1). This result is the net cash inflow or outflow in that particular month.

Step 8: determine your closing cash balance

Take the cash you have on hand (step 5) plus or minus your net cash flow (step 7) to determine your closing cash balance. Note: check to make sure that this amount equals the money you have in cash and in your bank account.

Step 9: use the results to manage your business

What do you see? What is your business telling you?

Using cash flow forecasting to manage your business

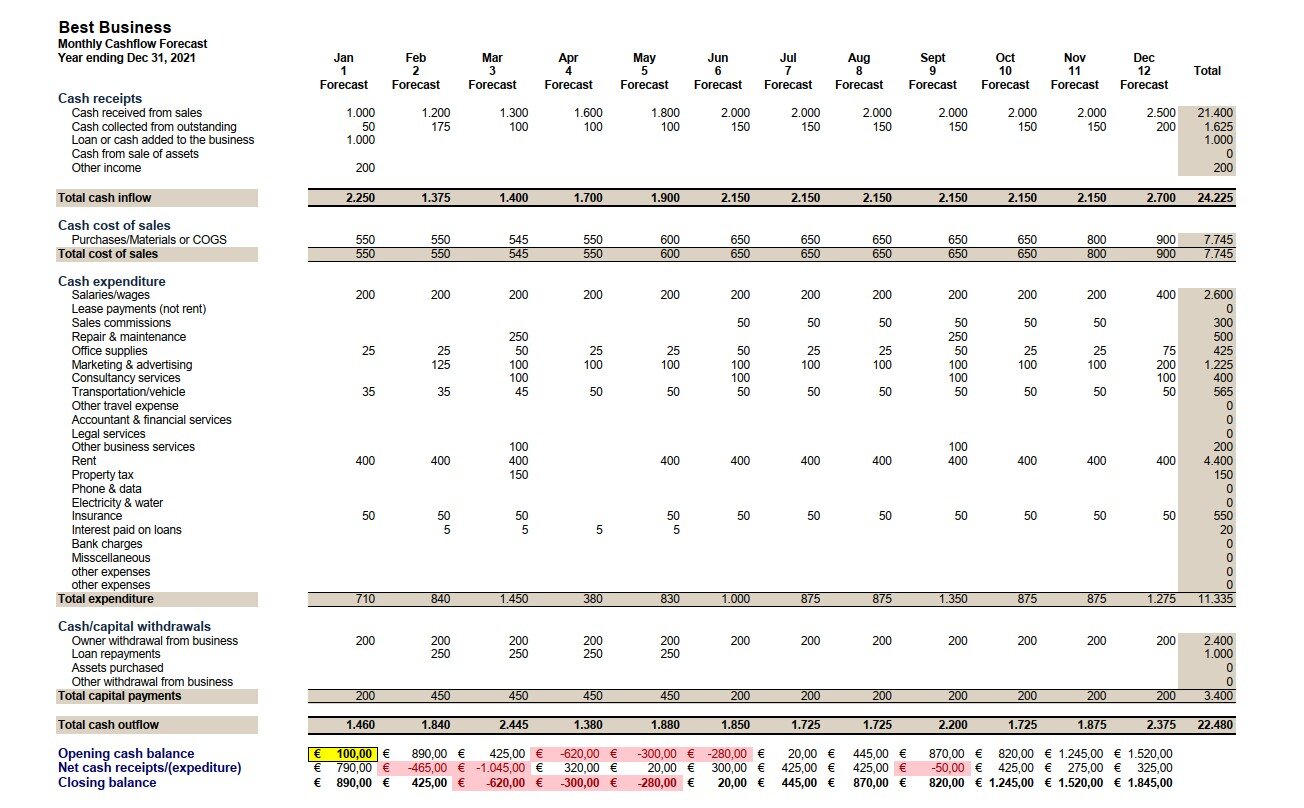

This is an example using a template that I created for small businesses in developing countries. Let us take a look at the cash flow of this fictional business. You can click on the picture to enlarge it or download it.

Cash inflow

The total cash inflow in increasing every month because sales are forecast to grow.

If I see this, I also expect the entrepreneur to have a strong sales strategy in place that is bringing in new customers or to be using one of these strategies to increase sales without spending additional money.

We also see that in January, this business received a 1000 loan and had other income of 200.

Cost of sales

The cost of sales is increasing as sales increase, but it is under control.

This tells me that the entrepreneur has an efficient manufacturing process or – if it is a retailer – the business owner has good control of prices of the goods he/she is buying.

Total expenditure

I’m seeing high expenses in March, September and December and very low expenses in April.

First of all, this tells me that this business needs to have higher cash inflows in March, September and December to cover the higher cash outflow. For example: sales should be much higher in these months. So, hopefully, the business owner has a good marketing strategy in place. Or, the entrepreneur should have financial reserves to be able to cover the higher expenses.

Secondly, the low amount of expenses in April tells me that the entrepreneur should be able to save a good amount of money in this month to build up financial reserves.

Cash/capital withdrawals

These are stable, the forecast is the same for every month.

It tells me that the business owner is careful not to take too much money out of the business. He/she also does not allow other people to take money out.

I note that the entrepreneur is repaying the business loan in 4 months (4x 250) and the interest on the loan has been recorded as a business expense. Well done.

Cash outflow

In this business, the lowest cash outflows are in January and April. The highest cash outflow is in March, followed by December and then September.

In February, March, and September the total cash outflow is higher than the total cash inflow. This is not a problem in February because the business owner has enough cash at the end of January to cover the shortfall. The same in September.

But in March (- 620), April (-300) and May (-280), the cash position is negative. Meaning that during these 3 months, the entrepreneur needs to have additional cash flowing in to cover the expenses. If not, he will struggle to keep this business alive.

If it is not possible to increase cash inflow, the entrepreneur will have to look for ways to reduce the expenses. For example: by paying certain expenses in instalments instead of the full amount. Or, by pushing some expenses to another month when the business has more cash coming in.

Click here to use this cash flow forecasting template for your own business

Conclusion

This business is profitable and is doing well. Starting from June, this entrepreneur does not expect to have any cash flow problems this year. In fact, starting from July, the cash flow is so high that this entrepreneur can save money to build financial reserves. Or use the money to invest for business growth.

However, there are 3 months this year that will be highly challenging for the business: March, April and May. The entrepreneur needs to find a way to deal with these 3 months. If not, the business may not survive.

So what can the business owner do?

Reduce costs or increase sales. Where can he/she reduce costs? Look at March. I am seeing additional costs which include:

- Repair & maintenance

- Consultancy services

- Other business services and

- Property tax payment.

One way to reduce the cash flowing out in March is to push these expenses to other months. The cash balance may still not be positive, but the amount the entrepreneur needs to find will be reduced.

However: if the entrepreneur cannot find a way to reduce costs, spread expenses or get additional cash this business will not survive the month of March even though the business is profitable.

You see? This is how cash flow problems can kill your business even if it is profitable.

Make sure to avoid that situation by using a good cash flow forecasting format, like this one

Avoid that situation by using a good cash flow forecast , like this one